Why Cheap Insurance Costs More Later | PolicyEra

Cheap insurance may save money today but cost lakhs later. Learn the hidden risks, coverage gaps, and choose smarter insurance with PolicyEra.

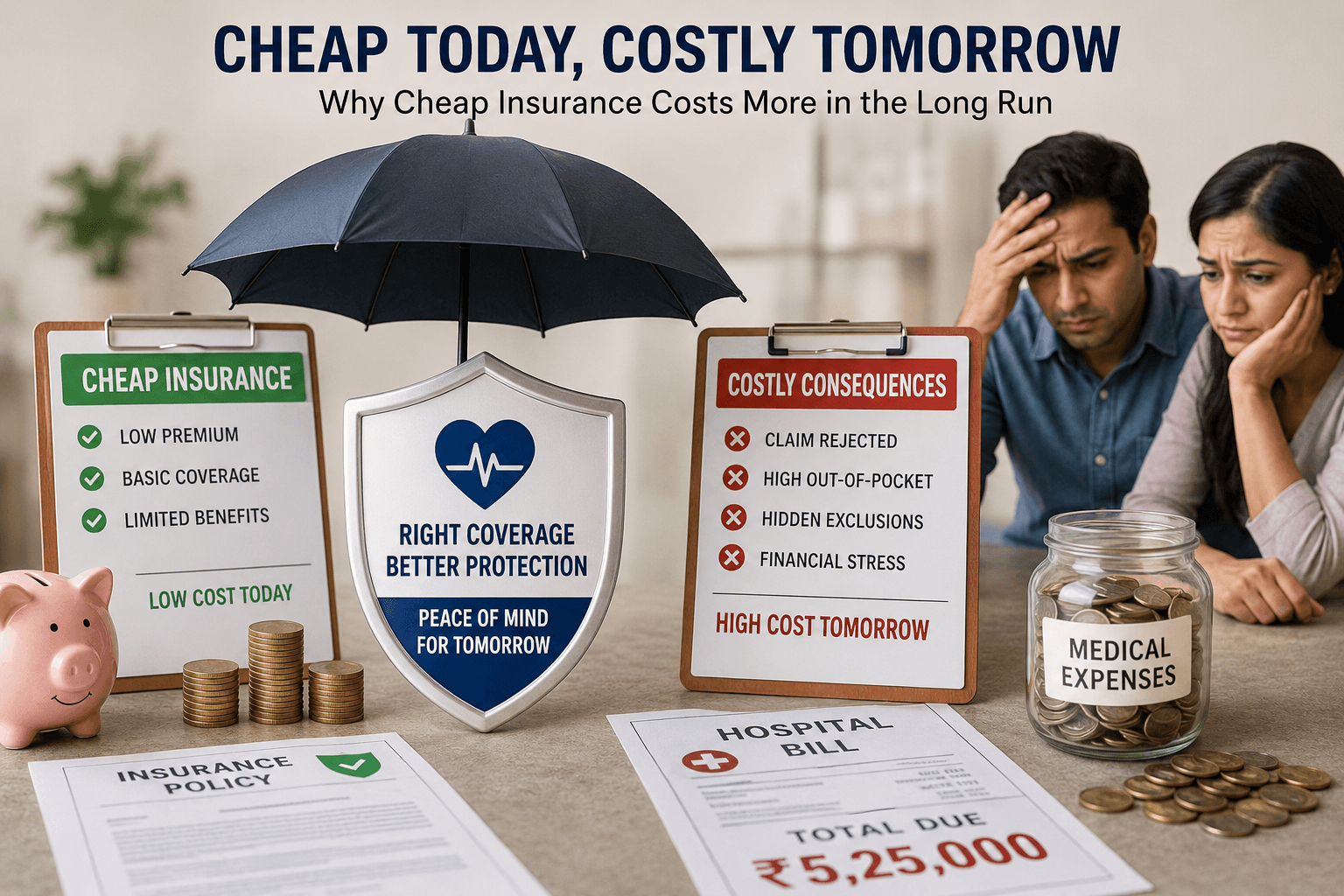

Why Cheap Insurance Costs More in the Long Run.png

Low Premiums Can Lead to Higher Costs Over Time

Some folks across India pick insurance mainly to save cash upfront. Looks clever at first glance, spending less now. Yet those bargain plans sometimes bring bigger bills later. Stress piles up when claims get denied. Hidden gaps in coverage lead to surprise expenses. Legal troubles can follow if terms aren’t fully understood. What seemed light on the wallet today may weigh heavily tomorrow.

Ever wonder why bargain coverage might backfire? Low prices on insurance often hide shaky protection beneath. Skipping thorough checks could leave you exposed when trouble hits. A smarter pick today means fewer headaches tomorrow. Finding solid value isn’t about cost alone - it’s what lies under the surface that counts.

The Illusion Of Low Premiums

Premiums that cost less catch attention, often helping those buying coverage for the first time or households watching every dollar. Yet what matters most isn’t price - it’s being ready when everything goes wrong.

When an insurer offers a very cheap policy, it usually means:

• Limited coverage • High exclusions • Strict claim conditions • Low claim settlement support

Yearly, you might keep two to five thousand rupees in your pocket. Yet when it comes time to file a claim, that saving could cost you anywhere between two lakhs and twenty lakhs. The lower premium today plays out very differently if trouble strikes tomorrow.

1. Inadequate Coverage Fails During Critical Times

Cheap insurance policies often come with:

• A tiny amount set for coverage. Not much protection at all • Room rent might have a cap. Surgery costs could be restricted too. ICU charges may face limits. Medicines often come with their own separate allowance • Disease-wise caps

Spending just five thousand rupees yearly feels light on the wallet. That three lakh cover might seem enough at first glance. Yet treatment in big cities often hits six to eight lakhs fast. When bills climb that high, money gets pulled from personal funds or borrowed. Protection on paper does not always shield reality.

At first glance seeming low cost, it ends up draining money down the line.

2. Hidden Exclusions and Fine Print Traps

Hidden gaps often live far down the page in cheap insurance plans

• Pre-existing diseases not covered for long periods • Some therapies won’t ever be covered. Certain medical approaches are left out without exception • Outpatient care might not cover certain day procedures. Some newer therapies fall outside standard benefits. Not every treatment option appears on the list • Waiting too long happens with childbirth care or operations Only after filing a claim do people notice their insurance won’t pay for the care they received.

3. High Co Pay and Deductibles

Some low-cost insurance plans come with these features:

• Each claim requires a required portion paid by you - between 10% and 30%. That share isn’t covered by insurance. You handle it yourself when billing happens • High deductibles

Even when approval comes through, out-of-pocket costs take up most of the expense.

A ₹4 lakh hospital bill means you cover ₹80,000 if there's a 20% co-pay.

4. Poor Claim Settlement Experience

Low‑premium insurers often cut costs by:

• Delaying claims • Need too many papers • Rejecting claims on technical grounds

A person facing hardship feels overwhelmed when their insurance adds worry instead of relief. Confusion builds quickly under money troubles, especially if help seems out of reach.

Here, low cost coverage often leads to heavy personal and monetary burdens.

5. Network Hospital Limitations

Some cheaper plans include these features

• Small hospital networks • Limited cashless facilities

Bills might need full payment right away when crises hit, leaving you to chase refunds afterward.

6. Renewability Drops and Premiums Rise Suddenly

Some cheap policies:

• Increase premiums sharply after claims • When policies renew, quietly cut back what they offer • At advanced ages, some still find their applications denied

Long-term insurance loses its point when things work out like this.

Why a Little Extra on Premiums Makes Sense

A well‑designed insurance policy offers:

• Adequate sum insured • Minimal exclusions • No co‑pay • Broad hospital network • Faster claim settlement

Spending an extra ₹1,500 to ₹3,000 yearly on a stronger policy might save you from facing bills worth ₹10 to ₹50 lakh down the line.

Policy Era helps avoid insurance mistakes

What matters most isn’t the lowest price tag on a plan - it’s how well it fits what you face every day. Coverage should match real life, not just look good on paper.

At Policyera.com, we:

• Start by looking at how old you are, who’s in your household, past health issues, what you earn, also where life might take you down the road.

• Look at several insurance options rather than focusing on just one provider.

• Start strong by picking plans that actually guard against risks, not merely ones with cheap prices. Sometimes the lowest cost brings little safety when trouble hits. Look beyond the sticker number into what gets covered if disaster strikes. Value shows up most when claims are filed, never before. Real security often hides behind slightly higher fees but pays back during emergencies.

How Policy Era Stands Out?

• Unbiased plan comparisons • Coverage‑first approach, not premium‑first • Transparent explanation of exclusions and waiting periods • Claim assistance support • Long‑term renewal and upgrade guidance

Staying safe now means fewer headaches later. What matters most? Handling things right from the start.

Final Thoughts

Skipping out on coverage now might feel smart. Yet down the road, that small saving could mean losing way more. When trouble hits, the math flips fast.

What seems like spending turns out to be protection. Money set aside today handles tomorrow's surprises.

Worried about what comes next? Good protection brings quiet thoughts during tough times. Picking plans that fit your life helps avoid stress later on. Clear advice matters most when choices feel confusing. Smart decisions today mean fewer surprises tomorrow.

Start smart by checking options at Policy Era. One choice might save more than you expect. Think twice before picking a plan - mistakes add up fast. Better details today mean fewer problems tomorrow. A small step now can prevent big bills later.

FAQs

1. Is Cheap Health Insurance Worth It in India

Cheap health insurance is worth considering only if it offers adequate coverage, fewer exclusions, and reliable claim support. Always compare policy benefits instead of choosing based only on a low premium.

2. Why Do Cheap Insurance Plans Reject Claims

Cheap insurance plans may reject claims because of policy exclusions, waiting periods, incomplete documents, or non disclosure of important information. Reading the policy terms carefully helps avoid claim issues.

3. Best Health Insurance Companies in India Customer Reviews

The best health insurance company depends on claim settlement, customer service, hospital network, and policy coverage. Customer reviews help understand the real experience before buying a policy.

4. Why Did My Insurance Claim Get Rejected

Insurance claims are often rejected because of non disclosure, policy exclusions, waiting periods, expired policies, or incorrect documents. Knowing your policy terms reduces the chances of claim rejection.

5. How to Appeal an Insurance Claim Denial

Review the reason for the claim denial, gather all required documents, and submit an appeal to your insurance company. If the issue is not resolved, you can raise a complaint through the grievance process.

6. What Should I Do If My Claim Is Denied

If your claim is denied, understand the reason, check your policy coverage, and provide any missing documents. Contact your insurer and follow the grievance process if further assistance is required.